Turkey Data Center Market

Regulated demand and improving interconnect

Bottom-up inventory, pipeline, power, and connectivity — neutral, source-backed view of Turkey’s DC market

Need to Know

Facts first; consequences embedded below charts

Colocation revenue guided near ~20% CAGR through 2030; Istanbul primary hub; Ankara/İzmir emerging. Treat all MW/price claims as verified-only.

Multiple subsea landings (Marmaris/Istanbul) and DE‑CIX Istanbul; AWS Direct Connect launched at Equinix IL4 in May 2025.

Installed capacity ~121.4 GW (Sep 2025); renewables rising. Climate workable with IEC/adiabatic; design for heatwaves; seismic design mandatory.

Executive Summary — House View

Thesis: Steady, regulated-led growth — not hyperscale-led (yet)

Attractive, steady-growth colo market with improving interconnect and rising regulated/hybrid demand; step‑change requires incentives + cable diversity + anchor commitments.

Demand: ~20% CAGR through 2030 with finance/public + hybrid cloud

Banking on‑shore rules anchor local hosting; KVKK cross‑border tools ease multinational hybrid; e‑commerce/media/gaming add latency‑sensitive load.

Supply: ~110–130 MW installed; ~150+ MW pipeline (Ankara‑weighted)

Istanbul remains interconnect center; Ankara pipeline includes Khazna (up to 100 MW) and Türksat (~21 MVA); İzmir adds Vodafone–EDGNEX program.

Connectivity & power: DX@IL4 + DE‑CIX now; KARDESA & TR‑EU backhaul next

Budget for tariff volatility with indexation/PPAs; interconnection timing at 154/380 kV is gating for RFS; market resilience improves with Black Sea route diversification.

Risk & design discipline

Climate workable with IEC/adiabatic; engineer for heatwaves; Istanbul↔Ankara active/DR for seismic diversity; keep IT MW vs facility MVA distinct; normalize program vs delivered MW.

Demand Drivers

What pulls capacity and where it goes

• Drivers inform siting and product mix; validate against account pipeline and sector rules.

Connectivity & Landings

Cable landings, IX presence, and cloud on‑ramps that shape siting

Subsea & Interconnection

- SEA‑ME‑WE‑5 — Marmaris (operator in TR: Türk Telekom)

- MedNautilus — Istanbul landing

- ITUR — Istanbul landing

- KAFOS — Istanbul–Varna–Mangalia (Black Sea)

- DE‑CIX Istanbul (carrier‑ and DC‑neutral exchange)

- AWS Direct Connect location at Equinix IL4 (10/100 Gbps, MACsec)

• SMW‑5 lists Marmaris (Türkiye) as a landing (Türk Telekom member).

• MedNautilus and ITUR list Istanbul landings; KAFOS connects Istanbul–Varna–Mangalia (Black Sea).

• DE‑CIX operates in Istanbul across multiple enabled sites; AWS Direct Connect opened at Equinix IL4 on 12 May 2025.

Upcoming route diversity (Black Sea)

Black Sea route diversity supports Istanbul/Ankara paths and Izmir adjacency; monitor execution and landing specifics for siting decisions.

• Vodafone announced the Kardesa Black Sea cable (Oct 20, 2025) with planned landings in Bulgaria, Türkiye, Georgia, and Ukraine; first landing targeted in 2027 (Bulgaria).

Power & Energy Context

Capacity, mix, and price context for budgeting

Capacity & Mix

Availability is improving and greening; grid interconnection timelines at 154/380 kV remain a siting critical path.

• Installed capacity reached ~121,418 MW by end‑Sep 2025; 61.6% renewables capacity share.

• 2024 generation shares: coal 34.7%, gas 18.9%, hydro 21.1%, wind 10.4%, solar 8.7%, geothermal 3.1% (Ministry).

• Akkuyu NPP Unit‑1 targets first power in 2025 (Reuters; officials).

Tariffs & Pricing (recent moves)

Budget with indexation/hedging; cross‑check wholesale exposure in contracts vs retail supply. Consider on‑site PV/PPAs where feasible.

• EPDK raised electricity tariffs effective 5 Apr 2025 (residential +25%; industrial +10%); BOTAS raised gas for industry (+20%) and power (+24.2%).

• Business retail benchmark ≈ $0.104/kWh (Mar 2025). Day‑ahead wholesale PTF averaged ~2,070–2,520 TL/MWh across 2024–3Q24; FX drives USD/kWh conversion.

Climate & Cooling

Thermal design ranges and extreme‑heat resilience

Operating envelope

Use IEC/adiabatic strategies with containment; expect higher summer PUE than Nordics; validate wet‑bulb and water strategy (WUE) per site.

• Istanbul typical July highs ~28–30 °C; inland Ankara cooler/drier — increases free/partial‑free cooling hours vs coast.

• Turkey set an all‑time national record of 50.5 °C (Silopi) on 25 Jul 2025; engineer for heatwaves, not means.

Seismic & Siting Notes

Marmara exposure and code context

Seismic probability & code

Prioritize modern stock, soil data, and isolation options; Istanbul clusters carry elevated seismic hazard vs Ankara.

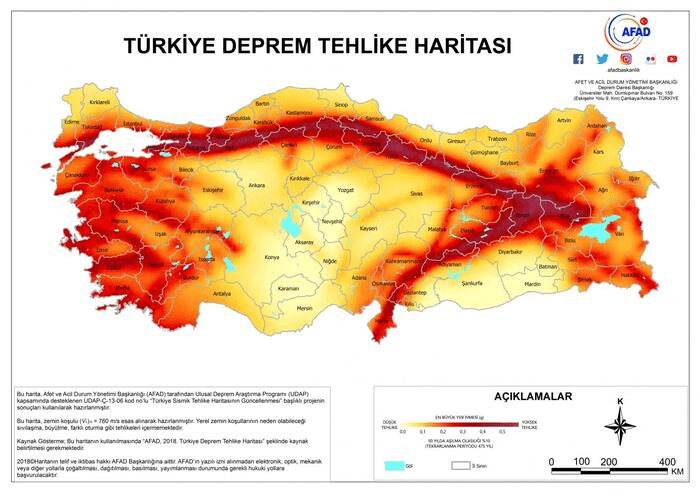

• USGS studies estimate ~40–60% probability of M≥7 event impacting Istanbul over 30 years (time‑dependent models).

• Apply TBDY‑2018 design and consider seismic isolation for critical facilities; confirm soil class and liquefaction risk per parcel.

Seismic risk map (AFAD)

• AFAD national seismic hazard map — for siting context only; perform parcel‑level geotech before decisions.

Regulatory Snapshot

KVKK cross-border tools; sectoral localization for banks

KVKK & Cross-Border Transfers (2024–25)

Practical: provide KVKK‑aligned standard contract templates and BCR language in your onboarding to ease multinational diligence.

• Türkiye is not in the EU/EEA; GDPR does not apply by law. KVKK (Law No. 6698) governs personal data.

• Amendments and secondary rules in mid‑2024 added GDPR‑style transfer tools: adequacy decisions, standard contracts (SCC‑like), and BCRs; 2025 guidance explains usage.

Banking (BRSA) — On‑shore Requirement

Play: target finance/public‑sector and hybrid adjacency (DX@IL4 + DE‑CIX). Offer Istanbul↔Ankara active/DR pairs for seismic diversity.

• BRSA rules require banks’ primary (and related outsourced/cloud) systems to be located in Türkiye. This materially anchors in‑country demand.

Istanbul vs Athens vs Crete

Cable diversity, IX/cloud adjacency, incentives, risk

Side‑by‑side (qualitative)

| Place | Cable diversity (within ~100 km) | IX / Cloud adjacency | Incentives / Policy | Headline risks |

|---|---|---|---|---|

| Istanbul | ITUR, MedNautilus, KAFOS; backhaul to SMW‑5 (Marmaris) | DE‑CIX live; AWS Direct Connect (IL4) | KVKK tooling; sectoral (BRSA) demand; standard investment regime | Seismic (Marmara); tariff volatility; EU jurisdiction gap |

| Athens | Med systems to GR; BlueMed paths to EU backbones | Cloud regions announced (MS/Google); large campus scaling | Strategic investment fast‑track; EU jurisdiction | Power siting queues; cost inflation |

| Crete | BlueMed landing; East‑Med route diversity | Edge to Athens; hub narrative forming | National push to make Crete a hub | Early‑stage; backhaul dependence to mainland |

• Greece has announced cloud regions (Microsoft/Google) and new East‑Med landings (BlueMed in Crete); Türkiye offers strong interconnect (DE‑CIX, DX@IL4) and evolving Black Sea diversity (KARDESA).

İzmir — Quick Diligence

Anchor colos vs boutique hosters

Operators and status

| Operator | Status | Published scale | Notes | Sources |

|---|---|---|---|---|

| Turkcell İzmir (Menderes/İTOB OSB) | Live | Purpose‑built Tier III; building ~14,500 m²; ~2,400 m² white space (press); MW N/A public | National‑scale telco DC; credible anchor in İzmir metro; verify current IT MW and interconnection details. | DCD — Turkcell launches İzmir DC |

| Vodafone Türkiye + EDGNEX (DAMAC) — İzmir | Announced | Program ~$100m; up to 6 MW (long‑term projection); phase‑1 target Q1 2025 | Treat $/MW as program‑level until delivered IT MW at COD disclosed; verify RFS status now. | Invest in Türkiye — announcement |

| Local hosting/ISP facilities (aggregated) | Live | Boutique/DC rooms; public MW typically not disclosed | Examples include PlusLayer, Alastyr, Inetmar, Netdirekt, Cenuta, Sağlayıcı, Websahibi, Hostegon. Treat as hosters/edge, not national‑scale neutral colos. | Data Center Map — İzmir listings |

• Treat boutique hosters as commercial presence, not proof of multi‑MW neutral colo; confirm MW and certifications before use.

Operators & Documented Capacity

Documented public figures (IT MW / white space)

| Operator | Metro | Site/Campus | Installed (IT MW) | Published Capacity | Status | Sources |

|---|---|---|---|---|---|---|

| Equinix — IL2 | Istanbul (Ümraniye, Dudullu OSB) | IL2 | — | 12,000 m² white space | Live | Equinix — acquires Istanbul DC from Zenium (2017), DCD — Equinix acquires Zenium Istanbul One (2017), Equinix — IL2 Istanbul IBX |

| Equinix — IL4 | Istanbul (Ümraniye, Dudullu OSB) | IL4 | — | — | Live | Equinix — IL4 Istanbul IBX, DE-CIX — Istanbul |

| NGN — Star of Bosphorus | Istanbul (Pendik) | — | — | 16.0 MW IT | Live | NGN — Star of Bosphorus Data Center |

| Radore | Istanbul (Levent, MetroCity) | — | — | 3.9 MW IT | Live | Radore — Data Center |

| Telehouse Istanbul (KDDI/Teknotel) | Istanbul (Kozyatağı) | — | — | — | Live | Telehouse Istanbul (KDDI/Teknotel) |

| Türk Telekom | Istanbul (Esenyurt, Gayrettepe) + Ankara (Ümitköy) | — | — | 12,700 m² white space | Live | Telehouse Istanbul (KDDI/Teknotel) |

| Turkcell (fleet) | Gebze, Ankara, İzmir, Tekirdağ | — | 33.0 MW IT | 54.0 MW IT | Live | Turkcell — Investor Presentation (Jan 2025) |

| KoçSistem | Istanbul | — | — | 3.3 MW IT | Live | Untes — KoçSistem Data Center (Istanbul) |

• Totals reflect published figures; treat values as indicative until verified via primary filings or operator pages.

• Avoid mixing facility MVA with IT MW; per‑rack specs are not directly comparable to sitewide MW.

Installed / published capacity (indicative)

• Only Turkcell reflects installed IT MW (33) from the Jan 2025 investor deck; other values are operator‑published site figures and may reflect facility or total capacity — treat as indicative / under review.

Pipeline & Announcements

Staged capacity and program capex (not delivered IT MW unless stated)

Comparability note

• Tip: Do not mix facility MVA with IT MW; label program totals separately from delivered first‑phase MW at COD.

Notable Program

| Sponsor/Operator | City | Stage | Capacity | Program Capex | Target COD |

|---|---|---|---|---|---|

| Vodafone Türkiye / EDGNEX (DAMAC) — 50/50 JV | İzmir (Aegean Region) | Announced | Up to 6 MW (program) | $100m | Q1 2025 |

| Khazna Data Centers | Ankara (Başkent OIZ) | Announced | Up to 100 MW (program) | — | — |

| Türksat | Ankara (near Gölbaşı) | Announced | 21 MVA facility power (initial phase); IT MW TBD | — | H1 2027 (target launch) |

• Implied capex intensity ≈ $16.7M per future MW assuming full 6 MW build; initial delivered MW at COD not disclosed.

• Do not compare program $/MW to realized IT MW benchmarks; harmonize on the same definition before comparison.

Pipeline / program totals (MW)

• Values shown as announced program totals. Türksat figure is facility MVA; Vod‑EDGNEX is ‘up to’ program MW; Khazna up to 100 MW. Not directly comparable to delivered IT MW at COD.

DC‑Relevant Incentives (Peer Snapshot)

What operators can actually bank on

Türkiye — Priority Investments & PBIS/HIT‑30

- Eligibility: ≥ 3 MW installed power; cloud DC spend ≥ TRY 200m

- Supports: VAT/customs exemption; tax reduction; social security; interest support; land allocation

- PBIS/HIT‑30: decree‑driven add‑ons (cashback, energy, capital contribution, etc.)

• Data centers are named Priority Investments with ≥ 3 MW installed power; cloud providers qualify with ≥ TRY 200m DC spend.

• Toolbox: VAT & customs exemption; tax reduction; social‑security support; interest/profit‑share support (capped); land allocation. PBIS/HIT‑30 can add cashback, energy support, capital contribution.

Greece — Fast‑Track & Development Law

- Fast‑track licensing (many permits ~45 days)

- Tax stabilization (up to 12y), accelerated depreciation, possible grants

• Fast‑track licensing windows; tax‑rate stabilization up to 12 years; accelerated depreciation; potential subsidies; strategic spatial planning tools.

Thailand — BOI (updated 2025)

- Up to 8‑year CIT holiday (no cap) for qualifying DCs

- Import duty exemptions; BOI one‑stop facilitation

• Up to 8‑year CIT exemption; import duty exemptions; 2025 updates add efficiency criteria and strategic packages.

Vietnam — Decision 29 & Telecom Law

- CIT 9%/30y; 7%/33y; 5%/37y (with exemptions/reductions)

- Land/water rent relief; large qualifying projects

• Special investment incentives grant deep, long‑tenor CIT holidays with exemptions/reductions; Telecom Law 2023 formalizes “data center services”.

Spain — national + regional mix

- National R&D/innovation credits; regional land/grid facilitation

• No single national DC holiday; operators combine national R&D credits/loans with regional facilitation and RES PPAs; grid investment rules evolving.

Peer Comparisons (Indicative)

Installed vs pipeline, on‑ramps, cables, power, regulation

Regional peers (qualitative only)

| Market | Installed (indicative) | Pipeline (indicative) | On‑ramps / Regions | Cables | Power Notes | Regulation |

|---|---|---|---|---|---|---|

| Türkiye | ≈110–130 MW documented colos (indicative) | ≈150 MW+ (Ankara-heavy; Türksat/Khazna; Vodafone‑EDGNEX İzmir) | AWS Direct Connect (IL4); DE‑CIX Istanbul; no hyperscaler region | SMW‑5 (Marmaris), ITUR, KAFOS, MedNautilus; KARDESA (Black Sea, 2027 target) | Tariff hikes Apr 2025; greening mix; interconnection timing key | Sectoral strict (finance) + KVKK transfers; broad consumer internet not blanket‑localized |

| Romania | Carrier hotels single‑digit MW per site (e.g., NXDATA‑3 ~5 MW total/3 MW IT) | HPC campus planned up to 200 MW (ClusterPower, Dolj) | No hyperscaler region; strong carrier‑neutral presence (Bucharest) | Terrestrial to EU backbones; Black Sea routes via RO‑BG; no major new subsea hub | Competitive power/PPAs vs Med; EU jurisdiction | EU GDPR; localization via sector or contractual needs |

| Bulgaria | Telepoint Sofia East ~9 MW; Neterra SDC2 ~2 MW (others 1–2 MW) | Incremental; retail/edge focus | No cloud region; Sofia carrier hotels active | Terrestrial to EU; Black Sea paths via BG‑TR‑RO | Competitive pricing; EU jurisdiction | EU GDPR |

| Serbia | Identified ~12 MW; ~6 MW live (Q4‑2023) | Small builds; selective wholesale | No region; limited on‑ramps; cross‑border adjacency | Terrestrial corridors; no subsea landings | Cost‑sensitive; check reliability hedges | Not EU; adequacy/transfer frameworks apply |

| Morocco | N+ONE Casablanca DC‑II ~4 MW; base small but growing | Announcements up to 500 MW (Dakhla) — treat as high‑risk until shovel‑ready | No region; emerging carrier‑neutral sites | Atlantic/Mediterranean routes; proximity to Iberia | RE growth; policy‑driven frameworks | Targeted localization for critical sectors |

| Thailand | ≈100–120 MW+ colos (indicative); large campuses in pipeline | 650 MW+ cited across Bangkok projects (indicative) | AWS Region GA (Jan 2025); other cloud regions announced | Multiple SEA cables via Thailand/Malaysia; terrestrial routes to SG/MY | BOI approvals; grid additions; price trends vary by tariff class | PDPA (since 2022); cross‑border transfer tools (adequacy/SCC‑like/BCR) |

Sources

- Invest in Türkiye — Vodafone & DAMAC announce İzmir DC

- Daily Sabah — $100m DC in Türkiye (media)

- AWS — Direct Connect Istanbul

- DE‑CIX Istanbul (official)

- Energy Ministry — Electricity (mix & capacity)

- Hürriyet Daily News — 121.4 GW (Ministry)

- Reuters — Apr 2025 tariff hikes

- GlobalPetrolPrices — business retail

- Weather‑Atlas — Istanbul climate

- DW — 50.5 °C national record

- USGS — Istanbul seismic probability (2000; 2016)

- USGS — Marmara probability (JGR 2016)